Proper recordkeeping is essential for every business, and the IRS requires accurate, complete, and organized financial records. Strong recordkeeping supports correct tax filings, protects you during audits, and helps you track business performance. This guide explains the IRS recordkeeping requirements and best practices for small and medium businesses.

Why IRS Recordkeeping Matters

- Prepare accurate tax returns

- Track income, expenses, and cash flow

- Claim valid deductions

- Support positions during IRS audits

- Avoid penalties for missing or inaccurate documentation

The IRS expects records that clearly show income, expenses, payroll, and asset information.

What Records You Need to Keep

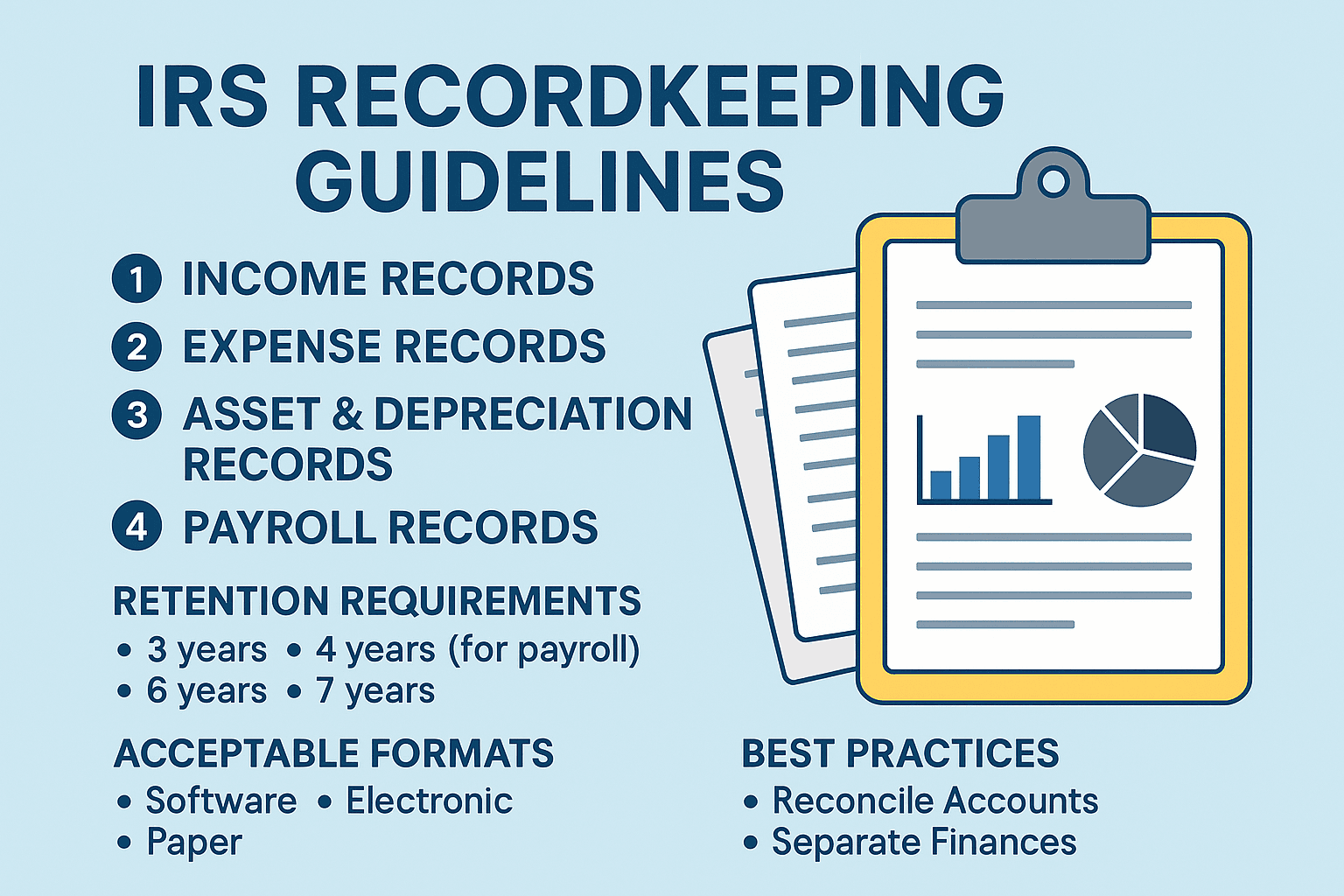

1. Income Records

Maintain proof of all income your business receives, including invoices, sales receipts, POS reports, bank deposit slips, merchant processor statements (Stripe, PayPal), and rental or contract income records. These must match the income reported on your tax return.

2. Expense and Deduction Records

Keep vendor invoices, receipts, subscription and software bills, utility bills, mileage logs, credit card statements, and equipment rental bills. Each record should show the date, amount, vendor, and business purpose.

3. Asset and Depreciation Records

For equipment, vehicles, or property, keep purchase invoices, loan documents, asset ledgers, depreciation schedules, and sale or disposal records. These support depreciation deductions and capital gains calculations.

4. Payroll Records

If you have employees, keep timesheets or hours worked, pay stubs, withholding records, payroll tax filings, and Forms W-2, W-3, W-4, and 1099-NEC. Payroll documentation must be kept for at least four years.

5. Banking and Financial Statements

Maintain bank statements, credit card statements, loan statements, investment summaries, and account reconciliations to verify the accuracy of your books.

IRS Record Retention Requirements

- 3 years: General tax records

- 4 years: Payroll tax records

- 6 years: Records for substantial underreported income

- 7 years: Bad debt and loss claim records

- Indefinitely: Fraud or unfiled returns, and asset/property records until disposal plus the return year

A safe standard is to keep tax documents for at least seven years.

Acceptable Recordkeeping Formats

The IRS accepts both paper and electronic records, including QuickBooks, Xero, and Zoho Books, digital copies (PDFs and scans), cloud storage, and paper files. Digital records are easier to search and store, but always keep backups.

What Happens if Records Are Missing

If you cannot produce records during an IRS review, deductions may be denied, tax liability may increase, penalties and interest may apply, and refund claims can be rejected. Strong recordkeeping prevents these risks.

Best Practices to Stay IRS-Compliant

- Reconcile accounts monthly

- Maintain separate business and personal accounts

- Save digital receipts for every transaction

- Track income and expenses in accounting software

- Document business purpose for deductions

- Review records quarterly

Helpful Resources

Related Services from Big Accountants

Need help getting IRS-ready? Explore our services:

- Professional bookkeeping services

- Business tax filing services

- Payroll processing services

- Fractional CFO services

- Monthly close process

Get Audit-Ready Books

Big Accountants supports SMBs across the USA, Europe, the Middle East, and Australia with accurate bookkeeping, documentation review, and IRS-ready financial reporting.